Catherine Delahaye/DigitalVision via Getty Images

If I am ever in a coma, the first thing I want my friends to do is to put bonding oil in my hair.

Every winter, I train in Montecito, CA (I play baseball professionally). In 2022, I walked into a lawyer’s office on Coast Village Road, the main street of Montecito, in hopes to be connected with a particular baseball agency I was seeking representation from at the time. However, before I walked into the office, I noticed the door right next door had Olaplex Holdings, Inc. (NASDAQ:OLPX) written on its window.

I remember hearing about Olaplex, but I didn’t know it was a publicly traded company or that it was headquartered in Montecito until after I looked it up online and looked in front of me, respectively. At the time, the stock was about $25 per share and was too expensive based on fundamentals. So, I discarded the idea and completely forgot about it.

Fast-forward two years to present day, when a girl I know made that above joke in quotes.

Except it wasn’t a joke. She was being completely serious. I asked her why on Earth would hair oil be a priority at a time like that?

With a completely straight face, she said that she can’t look unattractive when she wakes up and that the bonding oil needs to be Olaplex Nº7, specifically.

Why is this such a crucial story to the bull thesis?

Fountain of Youth

For the past thousand years, women (and men) have sought after beauty and youthfulness. I would be willing to bet that in another thousand years, the same statement above will be rewritten in its exact form by another observational writer, perhaps even on Seeking Alpha.

While many beauty products come and go, the ones that stay are the ones which provide women with the fountain of youth. Any product which keeps the magic flowing will always be bought.

In comes Olaplex. A company that has 2.5 million followers on Instagram, is getting tagged in about one post every single minute, has hundreds of thousands of near 5-star reviews on Amazon, and is part of Ulta’s and Sephora’s best-selling hair products page. In fact, just google “is Olaplex worth it Reddit” and read some of the forums. Here’s an example; just read some of these comments from women on how Olaplex is “worth its weight in gold.”

The key to understanding why this company is so intriguing as an investor is because of how effectively it solves the problem of “how can I restore my youth” not “how can I repair my hair” like most analysts are making the mistake of doing.

Investors have to understand, Olaplex’s success has nothing to do with hair repair; that’s just a means to an end. It has everything to do with how its products restore beauty and youth. This is what analysts are missing – they keep focusing on symptom, not the cause (the underlying driver of behavior).

Olaplex’s Current Financial State

Olaplex stock has been decimated since its IPO, plummeting approximately 95% from its all-time high of $1.40 per share. This alarming decline can be attributed to a dramatic collapse in revenue. Two primary factors are responsible for the decline in revenue, which consequently brought the stock price down with it:

- An incident regarding women who reported their hair fell out using Olaplex products.

- Increased competition, forcing backlogs, promotions, and loss of sales to competitors.

The first thing we have to do before deciding if Olaplex is a sound investment is address both of these issues.

Hair Loss?

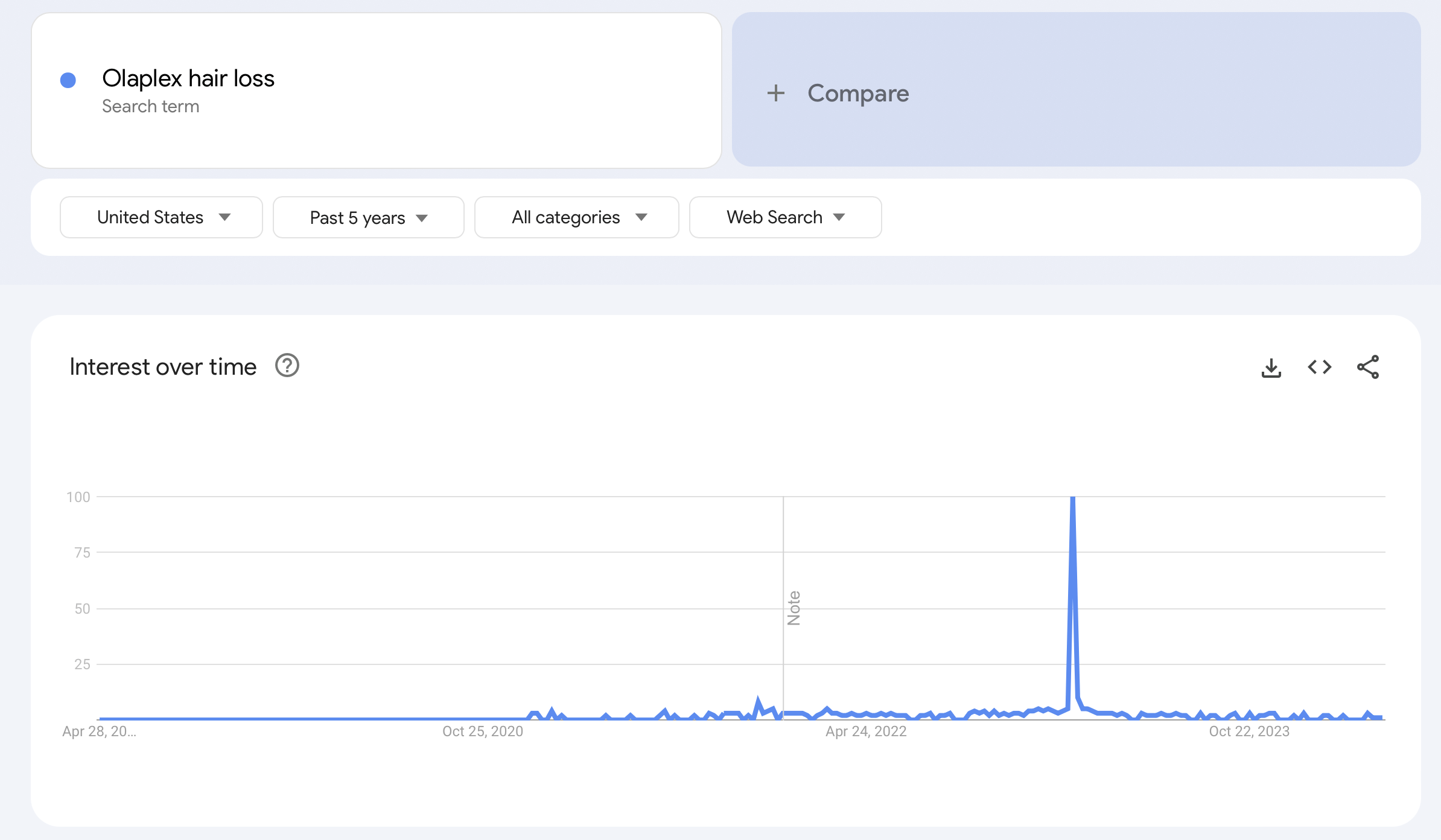

Around January 2023, Olaplex users started reporting hair loss after using Olaplex products. Relative to the company’s entire user base, few users were truly affected, but nevertheless, this incident was still damaging to the brand. The good news is that Google trends have shown that interest in “Olaplex hair loss” has returned to baseline and the comments on social media are positive across the board – no negative sentiment in sight about hair loss issues.

“Olaplex hair loss” Google Trends (Google Trends)

I feel confident saying this issue is in the past, but the brand damage has been done. The brand will never get those customers back, and some new customers will be deterred by the stigma of potentially losing their own hair.

Increased Competition

The hair industry thrives on evolving trends, with consumers constantly seeking novel and less mainstream products. With numerous new players entering the market, consumers are turning to alternative brands instead of Olaplex, resulting in a decline in revenue.

As a consequence, professional and specialty channels find themselves with excess inventory of Olaplex products due to the unexpected decline in demand. Consequently, Olaplex and its distributors are compelled to offer discounts to alleviate the backlog, further contributing to the revenue decline.

In the face of challenges posed by both the hair loss incident and heightened competition, it’s evident that the latter presents a more significant threat to Olaplex’s market position and financial stability.

So, what is Olaplex doing to maintain and gain market share?

Olaplex’s Plan

Olaplex is doing five things to reignite revenue growth.

Focusing on the Pro Community

Stylists are fickle, mostly due to their innate desire to constantly seek novelty, which, by the way, isn’t specific to stylists – it’s a part of us all as humans. Regarding the beauty industry, once a product becomes mainstream, many stylists want to find an alternative that is “new” and “exciting.” Olaplex, once synonymous with innovation, has lost some of its allure. To reignite stylists’ enthusiasm for the brand, Olaplex aims to adopt a more proactive approach. This includes providing new educational resources, increasing participation in trade show events, offering in-salon support through their education and sales team, and enhancing sampling efforts.

Will it work: While this strategy has the potential to succeed, it must be implemented with finesse. If perceived as an attempt to simply buy favor, stylists may reject it. Success lies in making each stylist genuinely feel valued, rather than merely being seen as a means to an end.

Ads and Marketing

Initially, Olaplex relied on genuine, unpaid social media campaigns, benefiting from users’ enthusiastic sharing of their positive experiences with the products. However, as this organic trend has waned, the company has found itself compelled to compensate with paid marketing efforts.

In 2023 alone, Olaplex allocated over $60 million towards marketing, a significant increase compared to previous years—marking a shift from $25 million in the preceding year and $11 million the year before that. With revenues standing at $458 million, $704 million, and $598 million for the respective years, the proportion of marketing expenditure relative to revenue has surged seven-fold from 1.8% in 2021 to 13.2% in 2023.

Will it work: While paid advertising may increase sales, it comes with a cost. Social media advertising, in particular, is pricey due to the fierce competition among brands all vying for the same consumer’s attention. This competition drives up advertising costs, which could lead to a permanent reduction Olaplex’s profit margins.

Reduced Promotional Activity

Olaplex expects to engage in less promotional activity compared to 2023, particularly in relation to clearing excess customer inventory. This shift may help maintain brand equity and profitability.

Will it work: While I anticipate this will relieve some of the downward pressure on revenue, I don’t foresee it leading to a substantial increase, either.

Product Innovation

Olaplex plans to continue its cadence of launching two to four new products per year. They aim to gain market share and increase sales with new products and product categories.

Will it work: I believe expanding the product offering is a great idea. Acquiring a new customer is more expensive than cross-selling or upselling among existing customers. I think expanding categories (skincare, nails, makeup) will be a primary driver of growth.

Market Expansion

The company is focusing on global expansion opportunities, leveraging the receptivity of the brand and its technology in 100 countries around the world.

Will it work: Similarly to new categories, new markets will also offer significant contribution towards future growth. Olaplex can rekindle some of the flame they once had in America among foreign countries, as the brand might still possess its novelty abroad.

Summary

Among the five options considered, I expect that reestablishing relationships with the professional community and reducing promotional activity will yield marginal results. The former is unlikely to resonate, given that stylists have shifted their focus elsewhere, and the latter represents a temporary fix—a mere “band-aid effect.” Moreover, any potential increase in sales resulting from these efforts may be offset by the increase in advertising costs, which will act as a drag on profitability growth.

However, the real growth potential lies in expanding into new categories and international markets. Here, Olaplex can capitalize on its established and loyal customer base by implementing strategies such as cross-selling, upselling, and tapping into emerging markets.

Let’s run through some different outcomes and see what the value of the business would be in each scenario.

Valuation

I will present a DCF for four scenarios (market, base, bull, bear) to help provide perspective on Olaplex’s fair value. I used the same starting point (revenue) for all my DCFs to be consistent and conservative.

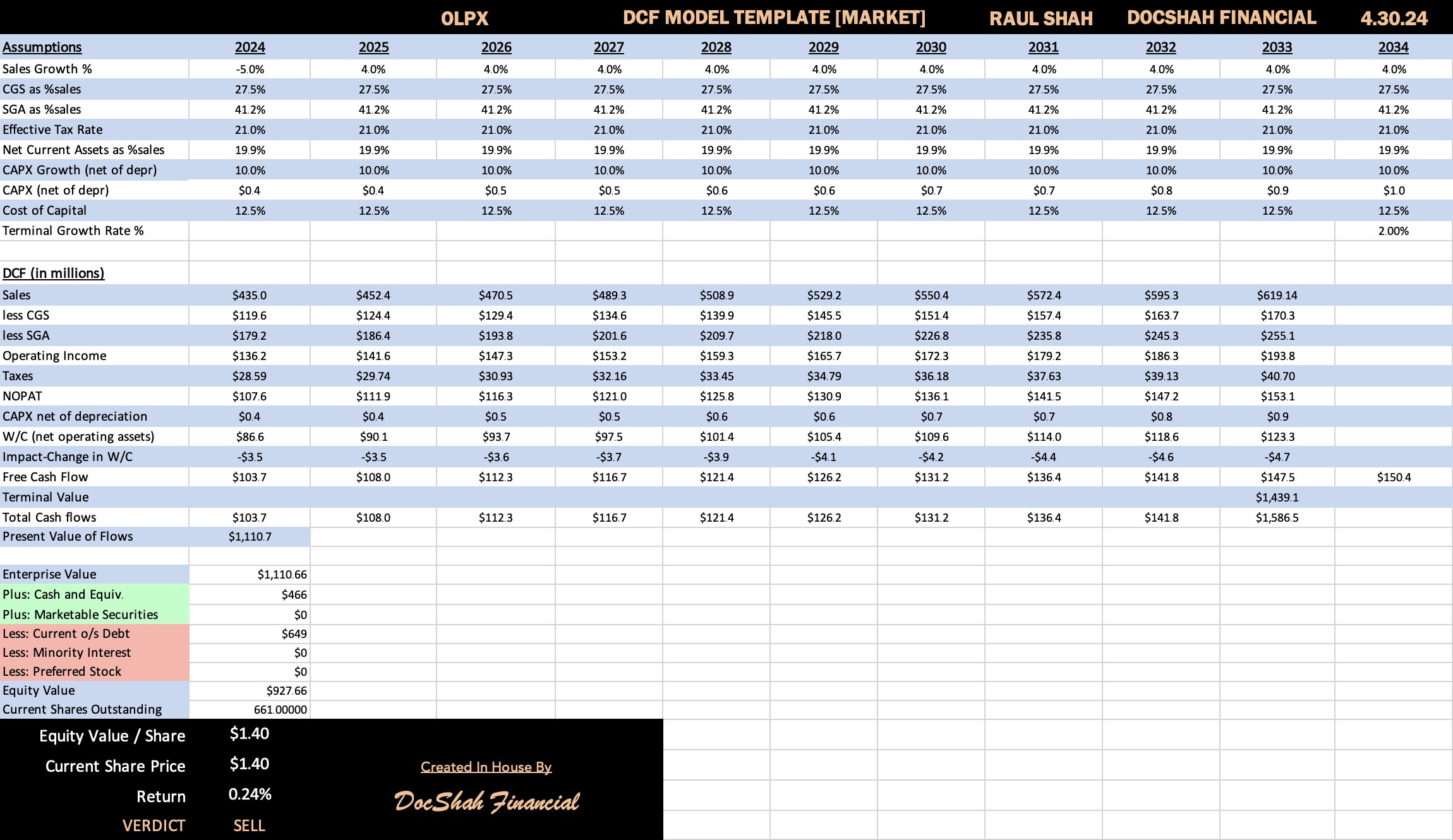

Market Case DCF

OLPX Market Case DCF (DocShah Financial (author))

Here are the important checkpoints to keep in mind for this DCF:

- Sales: I took the lower end of company guidance for 2024 ($435 million, range: $435MM to $463MM)

- Sales Growth: I assumed sales grow at 4%

- COGS: I took the lower end company guidance for gross margins (72.5%)

- SGA: I took the higher end of company guidance for SGA expense (179 million, range: $172MM – $179MM).

- WACC: Hand calculated to be 12.45%

- Terminal rate: Set to 2% to be conservative

- Misc: Everything else is based on historical averages and my own reasonable forward estimates

The reason this is the market case is that I wanted to see how the market is pricing this stock. The market is essentially saying that it expects Olaplex to grow revenue at about 4% per year for the next ten years, all else equal. In the market case, the fair share price would be the same as it stands today, $1.40.

How likely is this scenario? Due to stagnating growth and compressed margins, the current market price makes sense. However, I don’t think growth will remain stagnant. Let’s look at my base case.

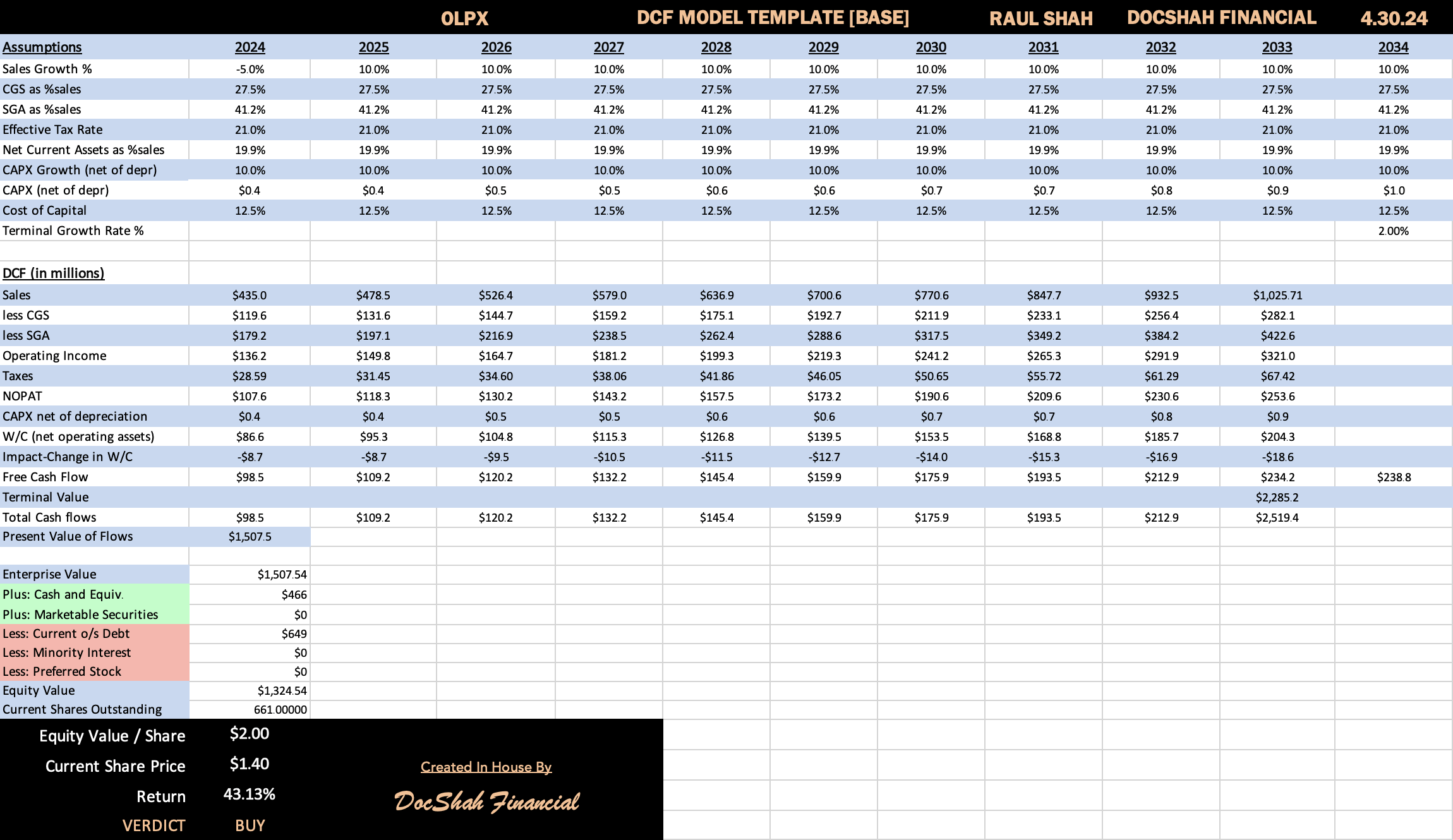

Base Case DCF

OLPX Base Case DCF (DocShah Financial (author))

The only thing I tweaked in my base case was that sales would grow by 10% a year instead of 4% in the market case. All other assumptions are the same. In the base case, the fair share price would be $2.00, which represents a 43% increase from current levels.

How likely is this scenario? I think the base case understates revenue growth. I believe that the initiatives the company is undertaking to reignite growth, particularly the new product launches and international expansion, will catch fire.

For example, if OLPX were to introduce a skincare line in 2025, it could potentially contribute a significant 5% increase to revenue, amounting to $24 million. Notably, the difference between projected revenue for 2025 and that of the previous year stands at $43.5 million. Therefore, the hair product line would only need to achieve a $19.5 million increase, representing a mere 4% of 2025 sales, for the skincare line to bridge the gap. This perspective helps understand the impact that product expansion could have on driving sales growth, particularly for a widely recognized brand like Olaplex.

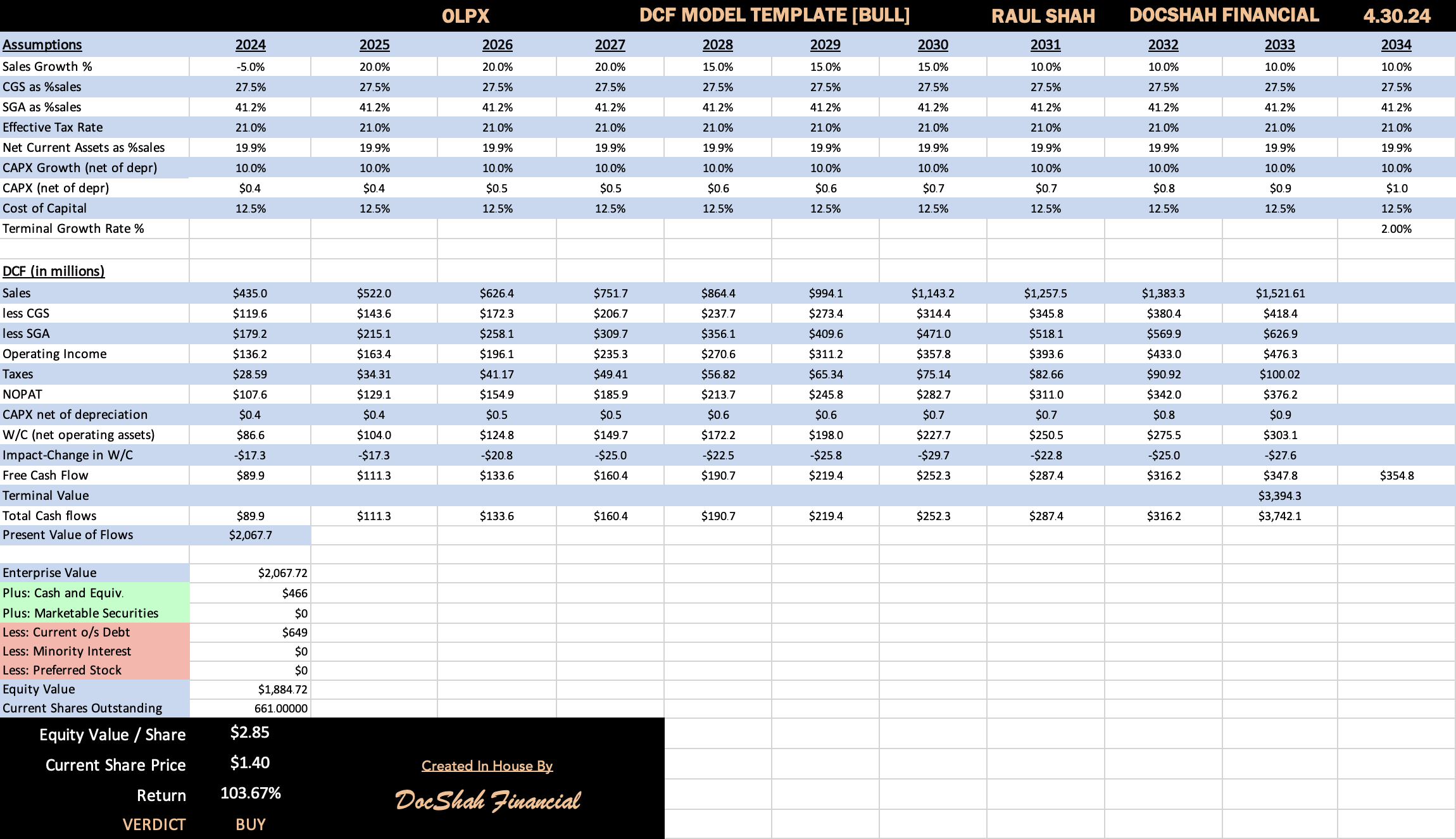

Bull Case DCF

OLPX Bull Case DCF (DocShah Financial (author))

The only thing I tweaked in my bull case was that sales would begin a rather quick (but still reasonable) ascent again. All other assumptions are the same. In the bull case, the fair share price would be $2.85, which represents a 104% increase from current levels.

The question now becomes how likely is this scenario? I believe my bull case will be the most likely outcome; the company would only be 3.5x bigger in ten years, which, I think, is a reasonable forecast. Olaplex, despite some brand damage, is still loved and used by millions of women and has incredibly strong brand power.

Investors who have given up on the stock most likely (1) overpaid years ago or (2) are using 2022 as a false baseline. If you compare any stock to its worst year, all the other years will look deceptively better. The same is true in reverse – if you compare a stock to its best year, all the other years will look deceptively worse.

OLPX’s high water mark revenue in 2022 was an anomaly.

If we remove that year, we will be able to see the facts more clearly. OLPX is a company that is:

- Profitable every year

- Cash flow from operations positive every year

- Free cash flow positive every year

- Solvent (all debt is covered with the cash on the balance sheet + FCF)

- Not reliant on fixed capital expenditures

- The market leader in numerous of its products (page 9)

- Extremely popular on social media (2.5MM followers on Instagram and getting tagged nonstop).

The market established unrealistic standards for this stock, leading many investors to jump ship due to unmet expectations. Is this solely the OLPX’s fault? Yes and no. While Olaplex bears responsibility for its stagnant growth, it’s important to recognize that the market’s lofty expectations are not entirely within the company’s control. Despite this setback, the company’s core operations remain robust, with a strong brand that resonates with women and products that outshine competitors. In fact, certain product categories lack direct competitors altogether, further underscoring Olaplex’s competitive edge.

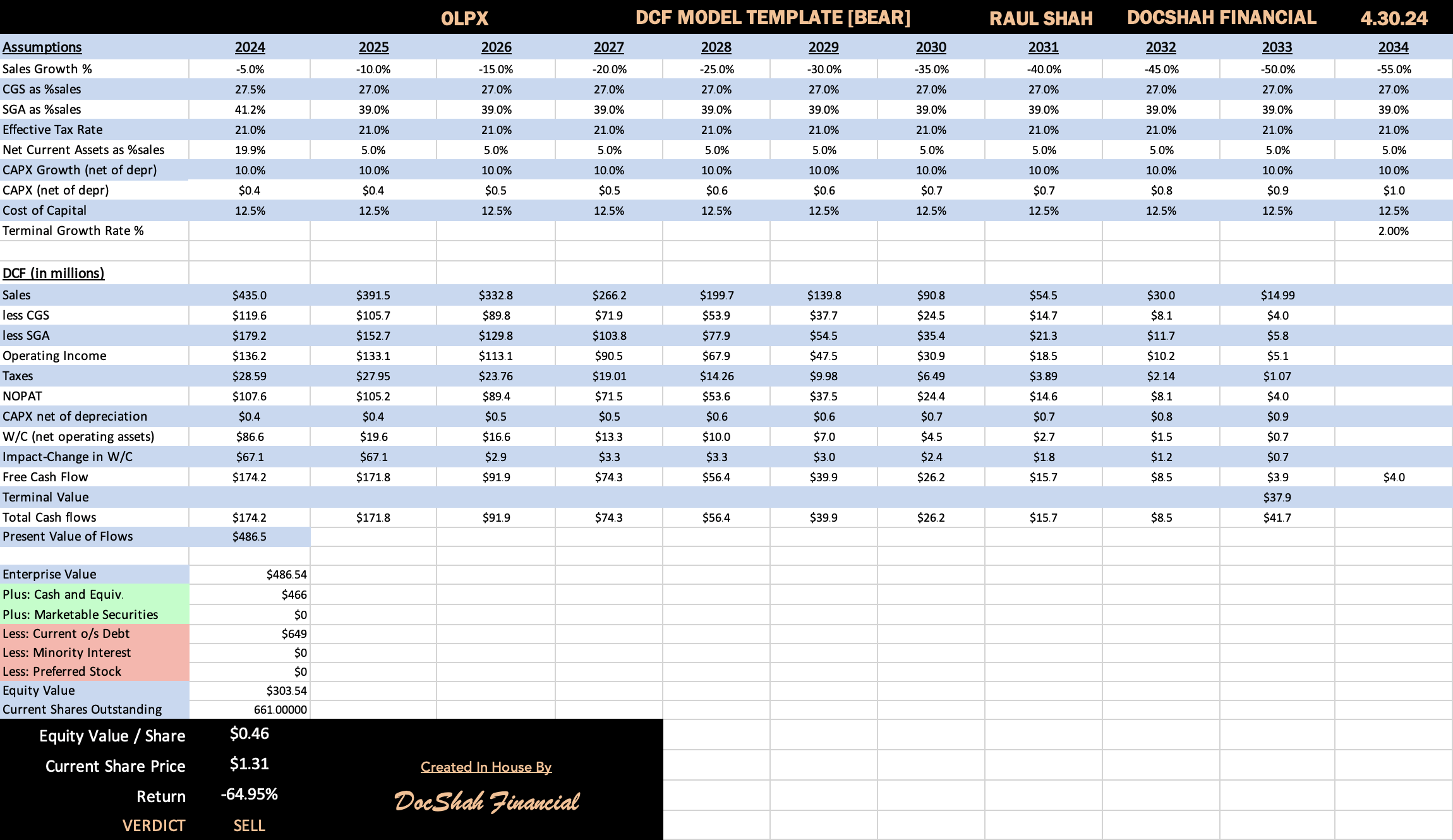

Bear Case DCF

OLPX Bear Case DCF (DocShah Financial (author))

The only thing I tweaked in my bear case was that sales would increasingly decrease. In the bear case, the fair share price would be 46¢, which represents a 65% decline from current levels.

The reason this is my bear case, is because I wanted to see what the stock price would be if revenue just entered into a free fall. The scenario in which this comes true is if Olaplex’s:

- Trends change and Olaplex falls out of favor as a brand

- Products become ineffective

- Patents expire and can’t fend off encroaching competition

- Advertising doesn’t reach its target demographic

- Plan to “butter up” stylists fails.

How likely is this scenario? I don’t foresee this happening. To put my bear case in perspective, sales in 2033 would be $15MM, which represents a 97% decline in demand (sales). I highly doubt 97% of Olaplex’s customers/revenue/demand are going to disappear, bar some completely unforeseen circumstance.

Risks

Olaplex has many challenging risks that investors need to consider.

- Concentration Risk: 80% of the shares are owned by Advent International.

- Consumer Sentiment Risk: Beauty products are trendy, and there’s no guarantee Olaplex remains popular.

- Product Risk: The market cap of the company is about $1 billion, which is objectively expensive for a company that only produces products in one category.

- Management Risk: Constant turnover of executives makes it difficult to build a culture.

- Concentration Risk: Over reliance on two customers, which represent 21% of sales (p. 11 10-K)

- Concentration Risk: Cosway Company Inc. manufactures products that accounted for more than 61% of net sales (p. 11 10-K)

- 10-K Risks: For the company’s set of risks, please click here.

Takeaway

Olaplex Holdings, Inc. stands at a crossroads. While its recent hair loss scandal and decreasing sales have cast a shadow over its solid operations, the company’s strong brand loyalty and innovative product offerings remain its core strengths. However, the real potential for Olaplex’s resurgence lies in expanding into new categories and international markets, where the company can leverage its existing customer base and capitalize on emerging opportunities. To me, it’s clear that Olaplex’s stock has intrinsic value far exceeding its current price, which is being obscured by negative market sentiment.