Vertigo3d

Oddity Tech (NASDAQ:ODD) is a consumer tech company that sells beauty products using a DTC model by leveraging machine learning, AI and other technologies. The company, which IPO’d in 2023 at $35 and is headquartered in Israel, is not only attractive because of its strategy to disrupt the behemoth beauty industry, but can also boast a promising valuation coupled with an impressive record of growth.

Beauty + AI + Data = Money?

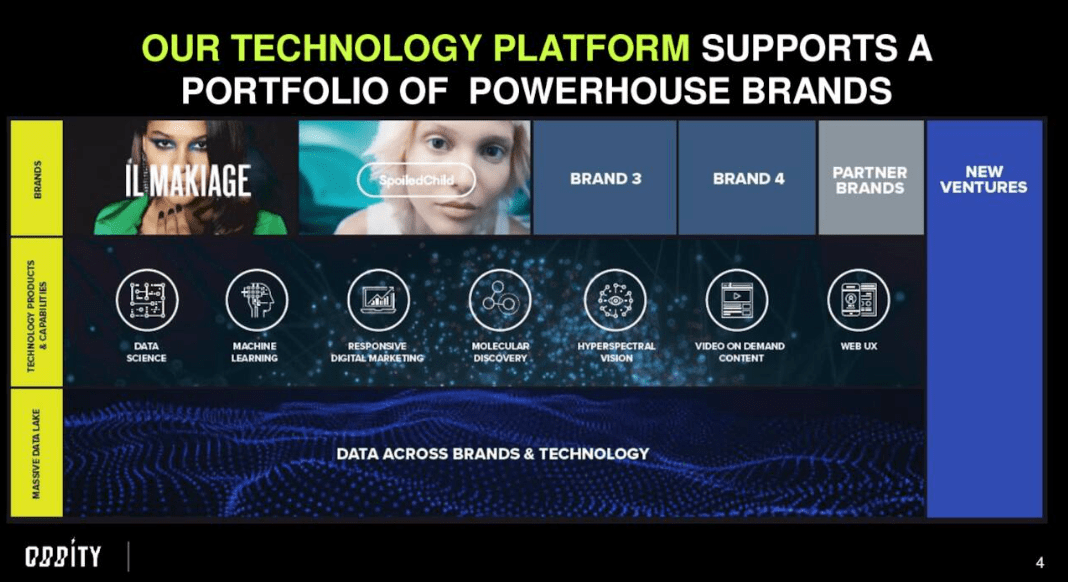

On initial inspection of Oddity, it might appear unclear whether it is a Tech company masquerading as a beauty company, or the reverse. Over 40% of employees are on the engineering, data science, or otherwise tech related side of things. Oddity’s website is aesthetically very tech, very AI, it’s only once you scroll to the very bottom—and that’s a lot of scrolling—do you see the actual beauty brands.

The company applies AI and data science to the beauty industry through their website, using AI to match customers and products, enabling a relatively personalised solution for different individual skin types. Computer vision further helps the matching process through hyperspectral imaging usable on normal smartphones, by analysing things like skin type and facial blood flow. The tech side of the business does not stop there though.

After a $76 million acquisition of Biotech start up Revela last year, Oddity can now develop products entirely from the ground, or rather molecule, up. Oddity Labs, their biotech lab based in the US, develops new molecules, peptides and probiotics using AI for molecular discovery. For example Fibroquin is a proprietary skin health molecule, which Oddity claims is superior to Retinol for improving skin elasticity while lacking some downsides. This type of research and development is common in the pharmaceutical industry but largely absent in the beauty industry. All of these systems seemingly leads to very high retention rates, with repeat revenue hitting more than 50% of revenue last year, and currently pushing much higher as the CFO outlines below.

Lindsay Drucker Mann, Q1 earnings:

Repeat rates continue to be very strong. We talked about last year it was more than 50% of our revenue, and in 2024 it’ll be even higher. In terms of 12-month net revenue repeat rate, we’ve talked about this 100%. So in other words, for a year ago, all of our first customers spent $100. Over the next twelve months, they spent an additional $100. And as far as we know, this is by far the highest repeat rate, 12-month net revenue repeat rate of any D2C, certainly that we’ve seen.

CEO Oran Holtzmann is not aiming to create customers you see, but users, and those numbers certainly help paint that picture. Statistics like that strongly validate management’s strategy and the unique vision of a fusion of beauty and tech, a fusion that seems to be paying off.

Q1

The quarter was great, revenue grew to $212 million, growing 28% YoY while EPS was $0.61, both beating expectations. In terms of outlook, EPS for the year meanwhile is expected to be between $1.57 and $1.62 and revenue for the year of $626 million to $635 million. In its relatively short history the company has a history of earnings beats coupled with impressive growth, so from their track record there is nothing to suggest the pace can’t be maintained.

Brands And TAM

For all the focus on the tech, it would be remiss not to mention the actual beauty products they sell. Currently Oddity has two brands, IL MAKIAGE and SpoiledChild. Both are digital beauty brands, with IL MAKIAGE having launched in 2018 and SpoiledChild more recently in 2022. IL MAKIAGE offers the usual array of cosmetics including foundations, eyeliners and lipsticks, as well as a growing skincare line, while SpoiledChild is more of a wellness brand offering hair and skincare products.

A third brand, currently referred to as Brand 3, is due to arrive next year according to management and will likely serve as a catalyst for the stock dependent on performance. Brand 3 is described as a ‘medical grade’ skin/body brand geared towards skin problems. This brand, similar to those before it, will leverage other systems like machine learning in conjunction with computer vision to help identify treatments. Oddity management is aiming for brands to be released around every 18 months, so it is critical that it succeeds.

Oddity Q1 earnings

The beauty industry as a whole represents a $600 billion TAM, while the skin care market is projected to reach $186 billion by 2028. Therefore, there is more than ample room available for the company to expand into, especially online beauty, as McKinsey notes E-commerce is the fastest growing segment of beauty products, interestingly also choosing wellness as a key theme in the same report, which would bode well for Oddity’s latest and coming brands. Further, with international revenues representing only 19% of revenue for 2023, there is plenty of room for expansion abroad, expansion which may prove easier as an online beauty company.

Valuation

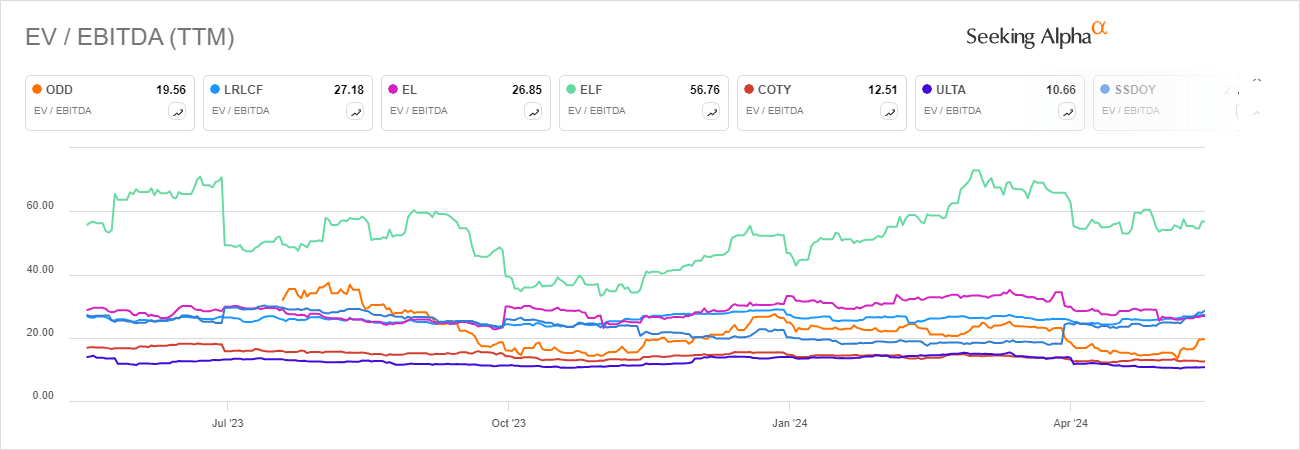

As a growth company it would be fair to expect valuation multiples above average, and compared to the sector they are, but drilling down into it, compared to other beauty companies Oddity’s multiples are perhaps surprisingly low. This is seen charted below, Oddity’s EV multiple is actually in a middling range excluding the outlier. On a forward basis that EV multiple drops to 15.84, about 46% above the sector median, while forward P/E is similarly 48.8% above the sector median. Despite these being well above average, the high growth more than explains it, in fact both the trailing and forward PEG ratios are over 40% below the sector median.

Seeking Alpha

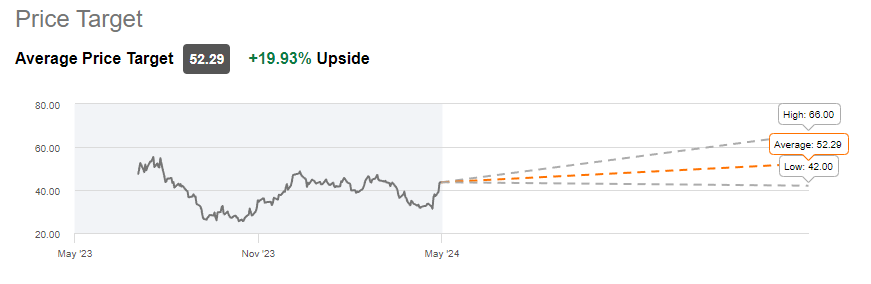

Wall Street’s current price target ranges seem to agree with the idea that the growth available here means there is room left to run for the stock with an average target sitting around $52.

Seeking Alpha

Risks

There could be some possibility of larger players in the industry adapting to a more similar model, either in terms of increasing online presence, which seems quite likely/inevitable, or even moving down a more science-based route for their products. At Oddity’s current size neither seems disastrous though because the scale of the TAM is quite large and, in these scenarios, Oddity would be ahead of the cofmpetition.

The combination of tech/pharma techniques and beauty is truly new, so inherently there is uncertainty there. Additionally, while online beauty is currently expanding, brick and mortar retailers are unlikely to disappear anytime soon so the rate of growth could slow. The numbers and performance so far definitely back up the story though, intuitively the strategy seems sound.

Lastly, with only two brands currently and at a cadence of years for new releases, the low number of brands means that they will be very vulnerable if one declines or does not perform.

Conclusion

Oddity so far is delivering on very ambitious objectives, blending growth and profitability just as surely as it does technology and beauty. In doing so it offers a unique way to play the trend towards online and a potential disruption to a massive industry. There are risks involved as with anything new and unknown and there has been a very recent spike in price after a stellar earnings report, for the latter reason I may refrain from immediately jumping in an attempt to time a better entry.